IPCC Study Highlights Role of Adaptation in Addressing Climate Risk

Max Dorfman, Research Writer, Triple-I (03/31/2022)

A recent report by the U.N.’s Intergovernmental Panel on Climate Change (IPCC) emphasizes the importance of “near-term mitigation and adaptation actions” to avoid the worst consequences of a warming world.

The IPCC report identified 127 main climate-related threats, which were analyzed in the mid- and long-term beyond 2040. It added, however, that the magnitude and rate of climate change and its associated risks depend heavily on near-term mitigation and adaptation.

“Adaptation plays a key role in reducing exposure and vulnerability to climate change,” the report says. “In human systems, adaptation can be anticipatory or reactive, as well as incremental and/or transformational.”

The report found that between 3.3 and 3.6 billion people currently live in settings that are extremely vulnerable to climate risk. As U.N. Secretary-General Antonio Guterres put it, “Nearly half of humanity is living in the danger zone – now.”

Insurers lead the way

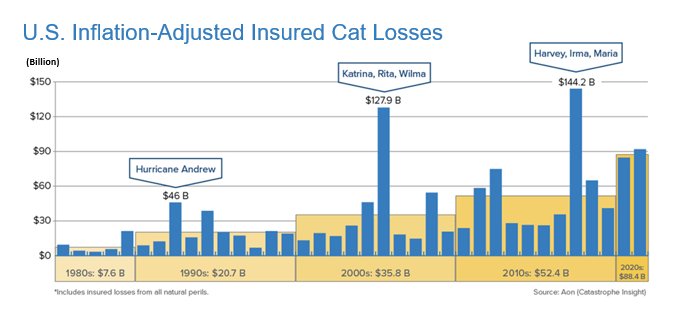

The insurance industry has been incorporating weather and climate into its analyses for decades.

“With industry loss costs related to natural catastrophes soaring nearly 700 percent since the 1980s, there can be no doubt that insurance has long been dealing with climate risk,” Triple-I CEO Sean Kevelighan recently told attendees at a National Council of Insurance Legislators (NCOIL) meeting. “With more people than ever moving to or living in catastrophe-prone areas, insurance is focused on helping customers and communities adapt to the changes, mitigate risks, and become more resilient.”

Risk transfer isn’t enough

Insurance is essential for individuals, businesses, and communities to recover quickly from catastrophes, but perils have evolved to the point that risk transfer alone is insufficient to ensure resilience. Better-insured communities recover more quickly than others, but “the long-term resilience of communities impacted by natural catastrophes and of the industry itself depend on preparedness and improved risk mitigation,” Kevelighan said.

The IPCC agrees that communities – along with the private sector, governments, and nations – must take be engaged in creating a world that is prepared.

The insurance industry has taken the lead on many of these issues. Insurers have been promoting the use of data and analytics tools to predict storms and pinpoint areas of concern, as well as strategies like community-based catastrophe insurance, which can spread the cost of insurance across communities for more effective and cost-efficient protection.

Some have gone further, involving themselves in efforts to attack climate risk at its roots. For example, members of the Net-Zero Insurance Alliance – a U.N.-convened group of insurers representing more than 11 percent of world premium volume – have committed to shift their insurance and reinsurance underwriting portfolios to net-zero greenhouse gas emissions by 2050.

Lloyd’s – the world’s largest insurance market – has said it will stop writing new coverage for coal-fired power plants, coalmines, oil sands, and Arctic energy exploration and to be out of the business of insuring fossil fuel operations by 2030, and members of the Glasgow Financial Alliance for Net Zero – which includes Axa, Allianz, Munich, and Zurich Insurance Group – have promised to “align their lending and investment portfolios with net-zero emissions by 2050.”

Insurers are also working to help communities recover faster. Parametric insurance, for example, pays claims based on verifiable parameters like rainfall or river level, without the need for costly, time-consuming, and frequently dangerous post-event claims adjusting. Instead of paying for damage that has occurred, a parametric policy pays if the agreed-upon conditions are met in a particular area. If coverage is triggered, a claim is quickly paid, regardless of damage.

Speed of payment and reduced administration costs can ease the burden on both insurers and policyholders. Alone, or as part of a package including indemnity coverage, parametric insurance can provide liquidity that businesses and communities need for post-catastrophe resilience.